That sharp, sudden toothache. The little wince when you drink something cold. Or maybe it’s just that quiet voice in your head reminding you you’ve been putting off a cleaning for… a while. We get it. Dental care is personal. But the cost side of it can feel confusing, stressful, and honestly a bit scary. 😬

If you’ve ever opened a treatment estimate and felt your stomach drop, you’re not being “dramatic.” That’s a very common reaction — and it makes perfect sense. Dental bills can show up at the worst time, and the numbers don’t always feel predictable. A lot of people end up doing the same thing: delaying care, hoping the problem magically disappears, and trying not to think about it.

Here’s our promise to you: this guide is a calm, clear conversation about a tool that can help you feel more in control. We’re going to walk you through, step-by-step, everything you need to know about finding the best dental savings plans for you and your family. We’re not dentists, but we are a team dedicated to helping you understand options, decode the costs, and choose with confidence. Take a breath. You’re in the right place. 💙

So, What Exactly Is a Dental Savings Plan? 🤔

Let’s start with the biggest point of confusion, because it trips up almost everyone at first. A dental savings plan (often called a dental discount plan) is not dental insurance. It’s simpler than that.

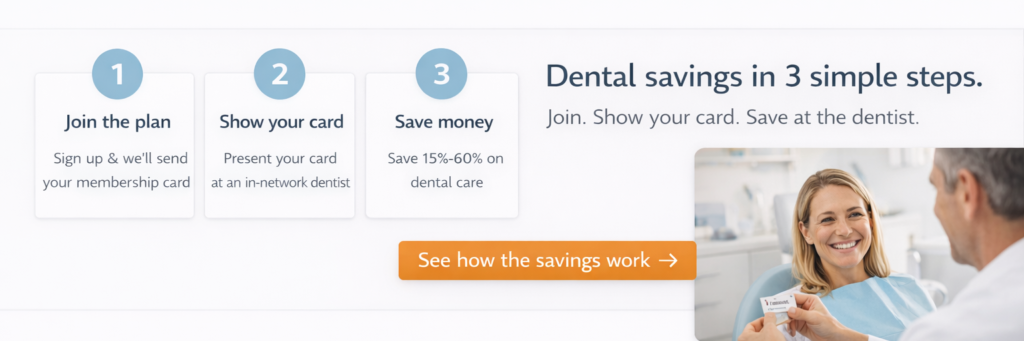

Think of it like a membership club for your teeth — kind of like Costco or Sam’s Club. You pay a membership fee (usually yearly). In return, you get access to discounted rates from a network of dentists who agree to offer members lower prices for specific services.

And here’s the part people love once they experience it: there’s usually no claim to file, no reimbursement to wait for, and no “we’ll see what gets covered.” You show your membership card at the dentist, and you pay the discounted price directly at the time of service. Clean. Simple. Transparent. ✨

If you’ve ever felt frustrated by insurance rules, that simplicity can feel like relief. Like, “Finally… I can just see the price and plan around it.” 😊

Another thing that matters emotionally (and practically): these plans are often designed for people who want help right now. No long forms. No confusing phone calls. No waiting months just to access basic benefits. For a lot of families, that feeling of “I can handle this” is a big deal. ❤️

Dental Savings Plans vs. Traditional Dental Insurance

Understanding the difference is the first step toward choosing what fits your life. It’s easy to mix them up — they both aim to reduce costs — but they work in very different ways.

| Feature | Dental Insurance | Dental Savings Plan |

|---|---|---|

| How It Works | You pay a monthly premium. The insurance company pays a portion of your dental bills after you meet your deductible. | You pay an annual membership fee. You get a discount on services at the time you pay the dentist. |

| Annual Maximum | Yes, typically $1,000 – $2,500. Once you hit this cap, you pay 100% of costs. | No annual maximums. You can use your discount as many times as you need throughout the year. ❤️ |

| Deductibles | Yes, you must pay a certain amount out-of-pocket before coverage kicks in. | No deductibles. Your savings start with your very first visit. |

| Waiting Periods | Often, yes. You may have to wait 6-12 months for major procedures like crowns or root canals. | No waiting periods. Most plans activate within a few business days, so you can start saving right away. |

| Paperwork/Claims | Yes, you or your dentist’s office must file claims for reimbursement. | No claim forms. Your discount is applied instantly at the dentist’s office. |

| Pre-existing Conditions | Some plans may not cover issues that existed before you enrolled. | Generally, all pre-existing conditions are included. |

| Cosmetic & Orthodontics | Often excluded or have limited coverage. | Many plans include discounts on cosmetic dentistry (like teeth whitening) and orthodontics. |

If you’ve been stuck in “insurance brain,” the biggest “aha” moments are usually these:

- No annual maximums (so you don’t suddenly lose help mid-year).

- No waiting periods (so you’re not trapped postponing care).

- No claim paperwork (so the process stays simple).

And if you’re thinking, “Okay… that already sounds less stressful,” that’s a normal response. 💬

How to Find the Best Dental Savings Plans for Your Needs

Now let’s make this real. Because understanding what a plan is… and choosing the best dental savings plans for your actual life are two different things.

And you deserve a plan that fits your situation — not a generic “best overall” label. That’s a very common worry (“What if I choose wrong?”), and it makes perfect sense. 😊

Here’s the good news: you can narrow this down with a few practical steps. No complicated strategy. Just a clear checklist that helps you avoid the most common mistakes.

Your Quick-Start Checklist for Choosing a Plan ✅

- Step 1: Assess Your Dental Needs (Present and Future)

Take a quick inventory. Are you mainly looking for savings on routine care like cleanings, exams, and X-rays? Or do you already suspect you’ll need bigger work — like a root canal, crown, extraction, denture, or implant? Does anyone in your family need braces?

This step matters because a plan that’s “great for cleanings” might not be the best if you already know you’re facing restorative care. And if you’re not sure what you need yet, that’s okay — many people start with preventive care, then decide once they have an exam. - Step 2: Check the Dentist Network (This is CRUCIAL)

A dental savings plan is only valuable if you can use it with a dentist you trust. Before you sign up, check which dentists near you accept the plan. A plan with no good local dentists isn’t a plan — it’s just a membership fee. 😬

Many people start by checking which dentists in their zip code accept a specific discount plan 💙. If you already have a dentist you like, call the office and ask which discount plans they accept. Office managers hear this question all the time. - Step 3: Look at the Fee Schedule

This is where the transparency can feel like a breath of fresh air. Most plans let you view a fee schedule before you join — a list of procedures and the member price.

It’s not just “up to 60% off.” It’s “this filling costs this much,” “this crown costs this much.” That’s what helps you plan and avoid surprises. ✨ - Step 4: Compare the Annual Fee to Your Potential Savings

Now we do simple math — nothing scary. ☕

If the plan costs around $100–$150 a year and saves you $80 per cleaning, two cleanings can already justify the membership. If you need a crown and save a few hundred dollars, the value becomes even more obvious.

The goal is to ask: “Will this plan realistically pay for itself this year?” - Step 5: Read the Fine Print

Good plans are clear about terms, activation, and refund policies. Look for any activation fees and understand how cancellation works.

This isn’t about being suspicious. It’s about being empowered. You deserve clarity.

One more gentle reminder: if you feel overwhelmed doing this alone, that’s normal. This stuff feels “financial,” and many people associate that with stress. But you’re already doing the right thing by learning how it works. 😊

Pro Insight: From the DentalSavings.cloud Team

We’ve reviewed countless plans and spoken with many users. The single biggest piece of advice we can offer is this: don’t just focus on the percentage discount. A plan that offers “up to 60% off” might sound best, but a different plan with a 40% discount on the specific procedure you need from your preferred dentist is infinitely more valuable. The best dental savings plans are the ones that align perfectly with your real-world needs. Always start with your dentist and your required treatments, then find the plan that fits.

A Closer Look at Popular and Trusted Plan Options

If you’ve been Googling, you’ve probably noticed something: there are a lot of plans. Like… a lot. 😬

That can make the whole thing feel harder than it needs to be. And if you’re thinking, “How do I know which ones are legit?” — that’s a very common concern. It makes perfect sense.

While hundreds of options exist, a few names consistently stand out because they’ve been around, they have large networks, and they’re widely recognized by dental offices. Let’s look at two of the most well-known examples so you can see what “real-world options” often look like.

The Careington CARE 500 Series Plan

This is one of the most established plans in the country. The Careington Care 500 discount dental plan is known for a broad provider network and strong discounts across many types of care.

- Great for: General dentistry, specialty care, and families.

- Highlights: Savings often range from 20% to 60% depending on the procedure and provider. Many people like that the plan can also include discounts on orthodontics and cosmetic procedures — categories insurance often limits or excludes. ✨

- Network Size: A large network can matter a lot if you move, travel, or want options beyond a single office.

A simple “real life” scenario: imagine you’re juggling family schedules, and you need a dentist with Saturday hours. A bigger network can increase the odds you can find someone nearby who fits your schedule and accepts your plan. That’s not a small thing. 💬

The Aetna Dental Access® Plan

Aetna is a household name, and their dental savings plan builds on that broad recognition. The Aetna Dental Access discount plan is another common choice because many dental offices already recognize the name, which can make conversations smoother.

- Great for: People who want a familiar brand and wide provider access.

- Highlights: Competitive discounts on preventive and restorative care, and often specialty care as well.

- User-Friendliness: Because it’s widely recognized, some offices can confirm acceptance quickly, which reduces friction and stress. 😊

If you’ve ever had the experience of calling an office and getting a hesitant “Umm… I’m not sure,” you know how stressful that can be. Familiar plans can reduce those awkward moments.

What Could Your Savings Actually Look Like?

Percentages are helpful, but actual dollar amounts are what help your brain breathe. 💙

Costs vary by state, city, and even the specific office. But here’s a sample table that illustrates what a discount plan might look like for common procedures.

| Dental Procedure | Average U.S. Cost (Without Plan) | Sample Discount (40%) | Your Estimated Cost (With Plan) | Your Estimated Savings |

|---|---|---|---|---|

| Adult Cleaning & Exam | $250 – $400 | $100 – $160 | $150 – $240 | $100 – $160 |

| Single-Surface Filling | $150 – $300 | $60 – $120 | $90 – $180 | $60 – $120 |

| Root Canal (Molar) | $1,200 – $2,000 | $480 – $800 | $720 – $1,200 | $480 – $800 |

| Porcelain Crown | $1,100 – $1,800 | $440 – $720 | $660 – $1,080 | $440 – $720 |

Disclaimer: These are estimates for educational purposes. Always check the specific fee schedule for your chosen plan and confirm costs with your dental office before treatment.

If you’re reading that crown line and thinking, “Wait… that’s a huge difference,” you’re not imagining it. For many people, a savings plan turns a “maybe someday” procedure into a “okay, I can do this” plan.

For a deeper dive into how these plans are structured, you can explore guides that explain how 1Dental plans work.

One more helpful mindset shift: you don’t need a plan that saves you money on everything. You need a plan that saves you money on the care you’re most likely to use. That’s the calm way to choose. 😊

Common Questions & Concerns About Dental Discount Plans

If you feel skeptical, good. Not in a cynical way — in a healthy “I want to understand what I’m buying” way. That’s a very normal instinct, and it makes perfect sense. 💬

Here are some of the most common questions people ask when they’re deciding whether dental savings plans are right for them.

“Is this too good to be true? What’s the catch?”

Totally fair question. The model works because it’s a win-win-win:

- You (the patient) win because you get immediate access to lower prices.

- The dentist wins because being listed in a network can bring them steady new patients. Dentists would often rather offer a discounted fee than leave schedule gaps.

- The plan administrator wins by collecting membership fees.

So there isn’t really a “catch.” It’s just a different model than insurance. Insurance pays part of the bill. A savings plan reduces the bill upfront.

If you’ve been burned by fine print before, it’s normal to assume something is hidden. That’s why checking the fee schedule and network first is so powerful. It gives you clarity before you commit. ✨

“Can I use a dental savings plan if I already have insurance?”

Usually, you can’t stack them on the same procedure at the same time. But people still combine them in practical ways, like:

- Using the savings plan for things insurance doesn’t cover, like cosmetic procedures or certain elective services.

- Using the savings plan after hitting the annual max on insurance.

This is a big one. If insurance stops contributing after a cap, a discount plan can still reduce your out-of-pocket cost.

If you’re unsure, call your dental office and ask how they handle it. You’re not the first person to ask, and it’s a normal question. 😊

“What if I need to see a specialist, like an orthodontist or an oral surgeon?”

Great question — and this is actually a strength of many dental savings plans. Many plans include in-network specialists like orthodontists, oral surgeons, endodontists, and periodontists.

The key is the same: confirm the specialist is in-network before your appointment.

If you’re not sure what type of specialist you even need, that’s common too. A lot of people just know “my gums hurt” or “this tooth is killing me,” not “I need an endodontist.” The American Dental Association (ADA) has a helpful overview of the roles of different dental specialists.

“Are there any dental needs these plans don’t cover?”

Savings plans are designed around services performed by licensed dentists and specialists. They’re generally not “coverage” in the insurance sense — they’re discounted professional fees.

One emerging area people ask about is at-home dental appliances. For things like custom-made night guards, retainers, or whitening trays, some people explore direct-to-consumer options. For instance, services like ihomedental allow you to get custom appliances using a mail-in impression kit, which can be a convenient and affordable alternative for those specific needs.

That said, it’s worth saying clearly: if you’re dealing with pain, swelling, bleeding, or anything that feels urgent, professional care matters. Even if a mail-in option is convenient, it’s not a replacement for a proper evaluation when symptoms are serious. 💙

“How fast can I actually use a plan?”

This is where many people feel relief. Unlike insurance, many dental savings plans don’t have waiting periods. Most activate quickly (often within a few business days), meaning you can use them soon.

If you’re reading this because you already have a dental issue happening right now, that urgency is real. And it makes perfect sense that you’d want an option that doesn’t force you to wait months just to get help. 😬

“How do I avoid choosing a plan that doesn’t really help me?”

This is one of the most important questions — and it’s where most people go wrong.

Here are three calm “avoid the headache” rules:

- Rule 1: Don’t choose based on the biggest discount number. Choose based on the procedures you’ll likely need.

- Rule 2: Don’t choose until you confirm real dentists near you accept the plan.

- Rule 3: Don’t assume your current dentist takes it — ask directly.

Picture this: you finally feel ready to book that cleaning, you buy a plan, and then you find out the closest in-network dentist is 45 minutes away. That’s frustrating. And it’s avoidable. A 2-minute network search first prevents that whole mess. 😊

Taking the Next Step with Confidence 😊

If you’ve made it this far, you’re already doing something important: you’re replacing uncertainty with clarity.

And if you’re thinking, “I just want to stop stressing about dental costs,” that’s not silly. That’s practical. That’s human. And it makes perfect sense. 💬

Here’s what you now understand:

- Dental savings plans are not insurance — they’re membership-based discounts.

- Many plans can be used quickly, without waiting periods.

- There’s often no annual maximum, which can be huge if you need more than just cleanings.

- The “best” plan is the one that matches your needs and the dentists you can actually see.

This isn’t about finding a magic solution. It’s about finding a tool that gives you control.

Imagine checking your budget and feeling less stressed because you’re not guessing anymore. Imagine booking an exam because you know the price won’t surprise you. Imagine getting the care you’ve been postponing — not because you suddenly “love dentistry,” but because it finally feels manageable. 💙

Whether you’re looking to save on a basic cleaning or major work, a good plan can be a steady support system. For many people, the next step is simply to find an affordable dentist in their area who accepts a quality plan, and suddenly, that path forward becomes real.

You have the knowledge now. You can compare options, check networks, and choose a plan that helps you protect both your smile and your finances. You’ve got this. ✨

Medical Disclaimer: Content on DentalSavings.cloud is for educational purposes only and not a substitute for examination or diagnosis by a licensed dentist. If you experience pain, swelling, or urgent dental symptoms, seek professional care immediately.

Affiliate Disclosure: DentalSavings.cloud participates in affiliate programs (including discount plan partners and other trusted partners). When you buy through our links, we may earn a small commission — at no extra cost to you. These partnerships help keep our guides accurate, independent, and free for readers.

© 2026 DentalSavings.cloud | All rights reserved.