Choosing between insurance and discount plans doesn’t have to be.

Feeling overwhelmed by dental costs? You’re definitely not alone. That moment when a treatment plan slides across the desk and your eyes jump straight to the total can feel like a small shock to the system. 😬 Your stomach tightens. Your mind races. How am I supposed to pay for this?

That reaction is incredibly common — and completely understandable.

For most people, the confusion quickly centers on one big comparison: dental discount plans vs dental insurance.

On paper, both promise savings. In reality, they work very differently, and those differences can seriously affect your budget, your timing, and your stress level. Add in unfamiliar terms like deductibles, annual maximums, and waiting periods, and it’s easy to feel stuck before you even start.

So let’s slow this down together. 💙

No pressure. No sales talk. Just a clear, calm walk-through in plain English.

Our role here isn’t clinical — we’re not dentists. Instead, we focus on helping people understand the financial side of dental care so they can make confident, informed choices. By the end of this guide, you’ll know exactly how these two options differ, when each one makes sense, and how to decide what fits your life, your needs, and your peace of mind. ❤️

What’s the Real Difference? Let’s Unpack It Together 😊

At first glance, dental discount plans and dental insurance seem to aim for the same goal: making dental care more affordable. But the way they get there is fundamentally different.

A simple analogy helps.

Dental insurance works a lot like car insurance. You pay a monthly premium whether you use it or not. When you need care, the insurance company steps in to pay part of the bill — but only after certain conditions are met. There are rules, limits, and fine print involved.

A dental discount plan, on the other hand, is more like a membership club — think Costco or Sam’s Club. You pay a membership fee, and that membership gives you access to reduced prices at participating dentists. There’s no middleman paying part of the bill. You simply pay a lower price directly to the dentist.

That distinction alone changes everything. Let’s look closer at each option so it really clicks. 🦷

Dental Insurance: The Traditional Route

Dental insurance is familiar, which can make it feel safer by default. But familiarity doesn’t always mean simplicity.

Here’s how it usually works.

You pay a monthly premium just to keep the policy active. Whether you see a dentist that month or not, that payment still goes out. When you do get treatment, your insurance helps cover part of the cost — but only after navigating a few layers.

Here are the most important terms you’ll encounter:

- Premium: The monthly fee you pay to maintain your insurance policy.

- Deductible: The amount you must pay out of pocket before insurance starts contributing. Preventive care is often excluded, but anything beyond that usually counts.

- Coinsurance / Copay: After the deductible, insurance pays a percentage of the bill — not all of it. If your plan covers 80%, you’re still responsible for the remaining 20%.

- Annual Maximum: This is a big one. It’s the total amount your insurance will pay in a year — often between $1,000 and $2,500. Once you hit it, you’re on your own for the rest of the year.

- Waiting Period: Many plans require you to wait 6–12 months before covering major procedures like crowns, bridges, or implants. That can be incredibly frustrating if you already know you need work done.

If you’ve ever thought, “I have insurance — why am I still paying so much?”, this is usually why. 😬

Dental Discount Plans: The Membership Approach

Dental discount plans strip away most of that complexity.

You’re not buying coverage. You’re buying access to pre-negotiated discounts. That’s it.

Here’s what defines a dental discount plan:

- Membership Fee: A low annual or monthly fee — often far less than insurance premiums.

- No Waiting Periods: This is huge. You can often sign up today and use the plan within days — sometimes even the next day.

- No Annual Limits: There’s no cap on how much you can save. If you need multiple procedures, the discounts keep applying.

- No Deductibles: Your savings start immediately, from dollar one.

- No Paperwork: No claims. No reimbursement forms. You show your membership card, the discount is applied, and you pay the reduced rate. ✨

Because these plans aren’t bound by insurance rules, they often include discounts on services insurance typically excludes — like cosmetic dentistry, whitening, veneers, and adult orthodontics.

For many people, that simplicity alone feels like a breath of fresh air. 💙

A Side-by-Side Look: Dental Discount Plans vs. Dental Insurance

Sometimes, seeing everything laid out side by side makes the differences unmistakably clear. Here’s a clean breakdown of dental discount plans vs dental insurance — and what each feature really means for you.

| Feature | Dental Insurance | Dental Discount Plan | What It Means For Your Wallet 💬 |

|---|---|---|---|

| How You Pay | Monthly premium (often $30–$80/person) | Annual or monthly membership fee (often $80–$200/year) | Insurance is a recurring monthly cost; plans are often a lower upfront expense. |

| How You Save | Insurance pays a percentage of the bill | You receive a percentage discount off standard fees | Shared cost vs. direct price reduction. |

| Waiting Periods | Common for major work (6–12 months) | Rare or nonexistent | Immediate access matters if you need care now. |

| Annual Limits | Yes — typically $1,000–$2,500 | None | Unlimited savings can matter a lot for bigger treatment plans. |

| Deductibles | Yes | No | No “pay first, save later” hurdle with discount plans. |

| Paperwork | Claims, approvals, explanations of benefits | None | Less hassle, fewer surprises. |

| Cosmetic Dentistry | Usually excluded | Often discounted | A big plus for whitening, veneers, or smile upgrades. |

| Orthodontics | Limited or requires add-ons | Commonly discounted | Helpful for adults and families alike. |

If this table makes you feel a little calmer already, that’s a good sign. 😊

Let’s Talk Real Numbers: A Common Scenario 🦷

Concepts are helpful, but numbers make things real.

Imagine Sarah needs a dental crown. Her dentist quotes $1,600. It’s not optional. And it’s definitely stressful.

Let’s walk through both options slowly.

Scenario 1: Using Dental Insurance

- Sarah has a $50 deductible and a $1,500 annual maximum.

- Her insurance covers crowns at 50% after the deductible.

- She pays the $50 deductible, leaving $1,550.

- Insurance covers 50%: $775.

- Sarah pays the remaining $775.

- Total out-of-pocket: $825.

But here’s the emotional catch: Sarah has now used over half of her annual maximum. If something else goes wrong this year, insurance may barely help — or not at all.

That uncertainty can linger in the back of your mind. 😬

Scenario 2: Using a Dental Discount Plan

- Sarah joins a plan with a $120 annual fee.

- The plan offers a 40% discount on crowns.

- The discount equals $640.

- Sarah pays $960 for the crown.

- Total out-of-pocket: $1,080.

At first glance, insurance looks cheaper for this single procedure. But here’s the emotional relief factor: there’s no annual cap. If Sarah needs another crown, a root canal, or even an implant later, the same discount applies again.

That predictability can be incredibly reassuring. ✨

If you want to understand exactly what happens from signup to savings, our guide on how dental savings plans work explains the process step by step.

Pro Insight: A Note From Our Research Team

One of the most common points of confusion we hear is the word coverage.

Insurance covers part of a bill. It’s a three-way relationship between you, your dentist, and the insurance company.

A discount plan reduces the bill itself. It’s a direct relationship between you and your dentist.

That difference matters. One involves sharing risk — and rules — with a third party. The other is about immediate, transparent pricing. Neither is universally better. They simply serve different needs.

So, Which One Is Right for Your Smile (and Wallet)?

This is the moment many people hope for a definitive answer — but the truth is gentler than that.

There is no universal winner in the dental discount plans vs dental insurance debate. The right choice depends on you.

Let’s look at common situations.

Dental Insurance Might Be a Good Fit If…

- Your employer heavily subsidizes it. If premiums are mostly covered, insurance can be very cost-effective.

- You mostly need preventive care. Cleanings, exams, and x-rays are often fully covered.

- You can plan ahead. Waiting periods are manageable if major work isn’t urgent.

- You like predictable monthly budgeting. Some people feel calmer with a set premium.

A Dental Discount Plan Might Be Your Best Friend If…

- You need care now. Pain doesn’t wait — and neither should you. 💙

- You’re self-employed, retired, or a student. Without employer help, insurance can be expensive.

- You expect major dental work. Implants, dentures, and multiple procedures can blow past insurance limits fast.

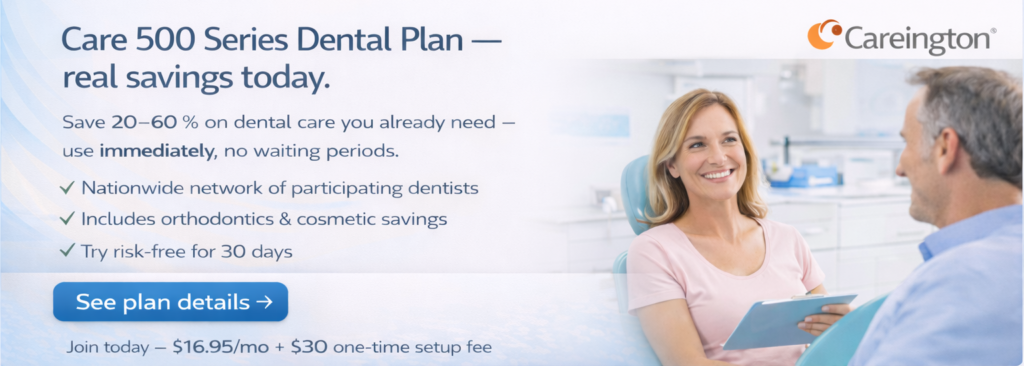

- You want cosmetic or orthodontic savings. Plans like the Careington Dental Plan often include both.

- You want simplicity. No claims. No approvals. No waiting.

Many people even use a discount plan after their insurance maxes out — a strategy that can significantly reduce unexpected expenses.

Your Action Plan: How to Choose with Confidence ✨

Let’s turn clarity into action. Grab a coffee. ☕ Take this one step at a time.

✅ Step 1: Assess Your Dental Needs

What do you need now? What might you need this year? Be honest. This step shapes everything.

✅ Step 2: Check Dentist Networks

Savings only matter if your dentist accepts the plan. Start by using tools to find a dentist near you who participates.

✅ Step 3: Do the Math

- Insurance: 12 months of premiums + deductible.

- Discount plan: annual membership fee.

Then compare estimated procedure savings.

✅ Step 4: Read the Details

Look at discount percentages or insurance coverage levels for the procedures you actually need.

✅ Step 5: Make a Quick Call

A simple confirmation call to the dentist’s office can prevent surprises later.

If you want help comparing options, our breakdown of the best dental savings plans is a great next step.

Safety, Trust, and Avoiding Surprises 💙

Feeling cautious here makes sense. Dental discount plans are legitimate, established programs — and they’re very clear that they are not insurance. That transparency is a good sign.

Look for large networks, clear pricing, and straightforward terms. And always remember: financial guidance is helpful, but clinical decisions should always come from a licensed dentist.

If you’re in pain or experiencing urgent symptoms, please seek professional care right away. ❤️

Your Path to Affordable Care Starts Now

The question of dental discount plans vs dental insurance isn’t about finding a secret trick.

It’s about clarity.

It’s about confidence.

It’s about choosing what fits your reality.

You now understand the trade-offs. You know the right questions to ask. And you’re far better equipped to make a choice that supports both your smile and your financial well-being.

Take a breath. You’ve got this. ✨

Medical Disclaimer: Content on DentalSavings.cloud is for educational purposes only and not a substitute for examination or diagnosis by a licensed dentist. If you experience pain, swelling, or urgent dental symptoms, seek professional care immediately.

Affiliate Disclosure: DentalSavings.cloud participates in affiliate programs (including discount plan partners and other trusted partners). When you buy through our links, we may earn a small commission — at no extra cost to you. These partnerships help keep our guides accurate, independent, and free for readers.

© 2026 DentalSavings.cloud | All rights reserved.